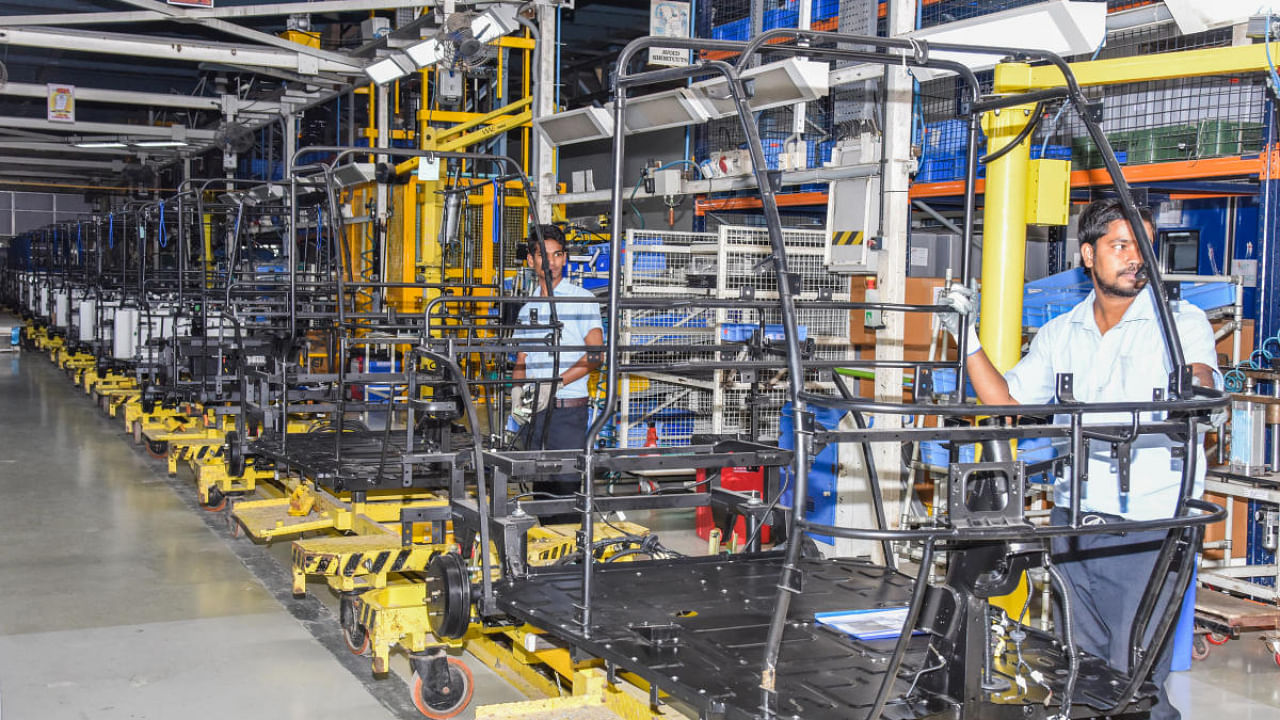

India’s manufacturing PMI came down marginally in September but continued to be in expansion mode for the 15th month in a row, signalling the strength of Asia’s third-largest economy amid global recession fears.

The S&P Global manufacturing Purchasing Managers’ Index (PMI) came at 55.1 in Sept versus 56.2 in August. A PMI above 50 denotes expansion and anything below that mark indicates contraction.

“The latest set of PMI data shows us that the Indian manufacturing industry remains in good shape, despite considerable global headwinds and recession fears elsewhere,” said Pollyanna De Lima, Economics Associate Director at S&P Global Market Intelligence.

“There were softer, but substantial, increases in new orders and production in September, with some indicators suggesting that output looks set to expand further at least in the short-term as firms seek to fulfil sales contracts and replenish stocks,” De Lima said.

According to the survey, companies hired extra employees and bought more raw material to accommodate higher sales and greater output needs. Employment rose at the quickest pace in three months.

“The PMI data remains strong complementing the cues provided by the data such as fuel consumption, rail freight and coal output,” said Aditi Nayar, chief economist, ICRA. Retail price inflation, which RBI tracks for its monetary policy making, came at 7 per cent in August. This was way above RBI’s upper limit of 6 per cent.

To tame rising prices, India’s central bank hiked its key policy lending rate by 50 basis points last week to 5.9 per cent, marking the fourth increase in a row in the past about five months.

“Once again, we saw businesses become more confident in the outlook as inflation worries were tamed,” Lima said.