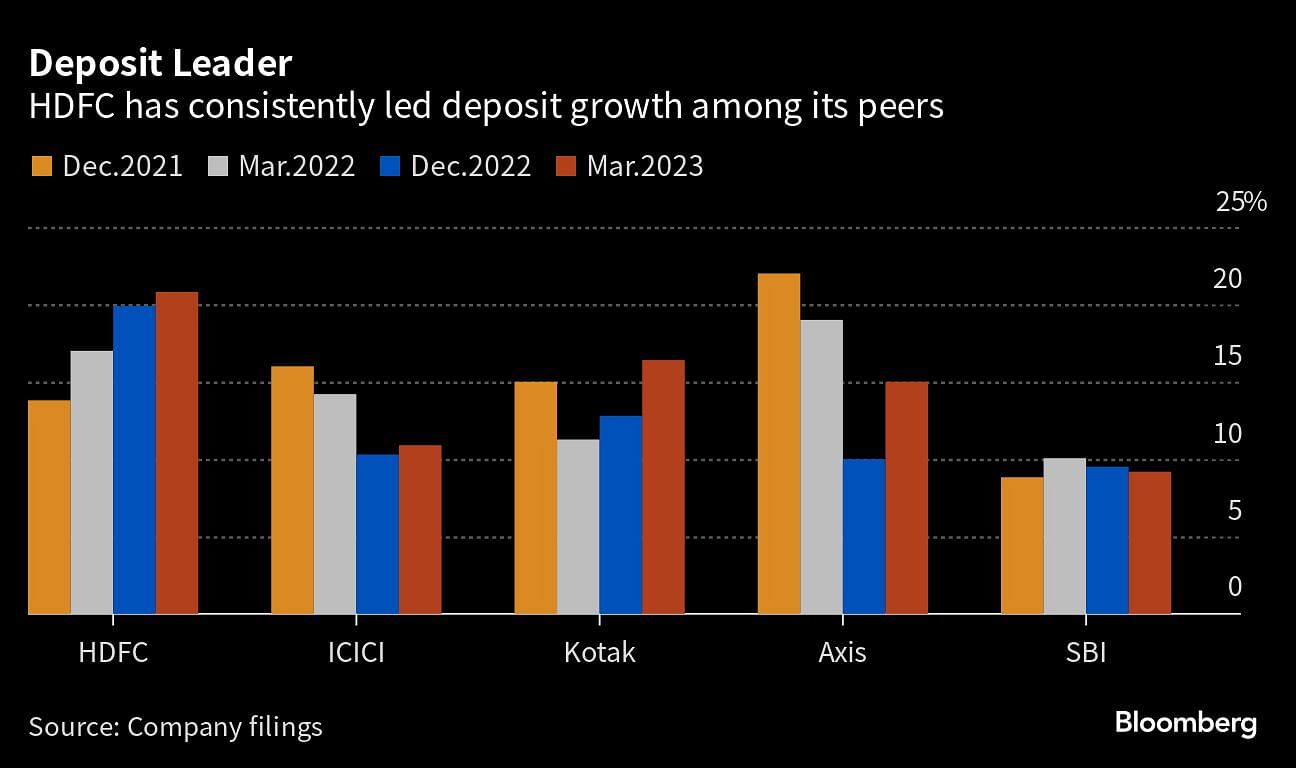

<p><em>By Preeti Singh and Divya Patil</em></p>.<p>A homegrown Indian company will for the first time rank among the world’s most valuable banks after completing a merger, marking a new challenger to the largest American and Chinese lenders occupying the coveted top spots. </p>.<p>The tieup of HDFC Bank Ltd and Housing Development Finance Corp creates a lender that ranks fourth in equity market capitalisation, behind JPMorgan Chase & Co, Industrial and Commercial Bank of China Ltd and Bank of America Corp, according to data compiled by <em>Bloomberg</em>. It’s valued at about $172 billion. </p>.<p><strong>Also read | <a href="https://www.deccanherald.com/business/business-news/hdfc-hdfc-bank-merger-to-be-effective-from-july-1-1231647.html" target="_blank">HDFC-HDFC Bank merger to be effective from July 1</a></strong></p>.<p>With the merger likely effective July 1, the new HDFC Bank entity will have around 120 million customers — that’s greater than the population of Germany. It will also increase its branch network to over 8,300 and boast of total headcount of more than 177,000 employees.</p>.<p>In the charts below, we highlight the scale of this global banking giant and examine some of the challenges ahead for its stock price. </p>.<p><strong>Market Capitalisation</strong> </p>.<p>HDFC surges ahead of banks including HSBC Holdings Plc and Citigroup Inc. The bank will also leave behind its Indian peers State Bank of India and ICICI Bank, with market capitalizations of about $62 billion and $79 billion, respectively, as of June 22. </p>.<p>“Worldwide there are very few banks, which can at this scale and size, still aspire to double over a period of four years,” Suresh Ganapathy, head of financial services research for India at Macquarie Group Ltd’s brokerage unit, said in a <em>Bloomberg TV </em>interview. The bank expects to grow at 18 per cent to 20 per cent, there is very good visibility in earnings growth, and they plan to double their branches in the next four years, he said. “HDFC Bank will remain a pretty formidable institution.”</p>.<p><strong>Deposit Growth</strong></p>.<p>HDFC Bank has consistently outperformed its peers in garnering deposits and the merger offers another chance to grow its deposit base by tapping the existing customers of the mortgage lender. Some 70 per cent of those customers do not have accounts with the bank. Arvind Kapil, retail head at the bank, last month said he plans to get them to open a savings account. </p>.<p>The lender will be able to offer inhouse home loan products to its clients as only 2 per cent of them had a mortgage product from HDFC Ltd, according to a presentation when the merger was announced.</p>.<p>“The lifetime value of a customer’s relationship with that bank just enhances when you start to put a mortgage into his product offering,” Sashi Jagdishan, the bank’s chief executive, said at the time. </p>.<p><strong>Confidence Check</strong></p>.<p>HDFC Bank, which counts JPMorgan among its largest investors, is enjoying high levels of investor confidence. Its contingent convertible bonds — the riskiest type of debt that can convert to equity if a lender runs into trouble — has outperformed its global peers. The perpetual dollar notes of HDFC Bank handed investors a return of 3.1 per cent so far this year, even as Bloomberg’s index of global banks’ coco bonds lost 3.5 per cent.</p>.<p>The aggregate index has clawed back some of of its underperformance in recent months after the turmoil caused by a controversial wipeout of Credit Suisse Group AG’s bonds eased. </p>.<p><strong>Stock Performance</strong></p>.<p>HDFC Bank shares are up less than the NIFTY Bank index over the past year. Ganapathy, the Macquarie analyst, reckons the stock’s performance will depend on the growth of the loan book at 18 per cent to 20 per cent, and a 2 per cent return on assets. </p>.<p>“Management is confident of sustaining 2 per cent return on assets and possibly beyond that level even post-merger and also deliver strong loan growth. If they can walk the talk, the stock will re-rate,” Ganapathy said in a note.</p>

<p><em>By Preeti Singh and Divya Patil</em></p>.<p>A homegrown Indian company will for the first time rank among the world’s most valuable banks after completing a merger, marking a new challenger to the largest American and Chinese lenders occupying the coveted top spots. </p>.<p>The tieup of HDFC Bank Ltd and Housing Development Finance Corp creates a lender that ranks fourth in equity market capitalisation, behind JPMorgan Chase & Co, Industrial and Commercial Bank of China Ltd and Bank of America Corp, according to data compiled by <em>Bloomberg</em>. It’s valued at about $172 billion. </p>.<p><strong>Also read | <a href="https://www.deccanherald.com/business/business-news/hdfc-hdfc-bank-merger-to-be-effective-from-july-1-1231647.html" target="_blank">HDFC-HDFC Bank merger to be effective from July 1</a></strong></p>.<p>With the merger likely effective July 1, the new HDFC Bank entity will have around 120 million customers — that’s greater than the population of Germany. It will also increase its branch network to over 8,300 and boast of total headcount of more than 177,000 employees.</p>.<p>In the charts below, we highlight the scale of this global banking giant and examine some of the challenges ahead for its stock price. </p>.<p><strong>Market Capitalisation</strong> </p>.<p>HDFC surges ahead of banks including HSBC Holdings Plc and Citigroup Inc. The bank will also leave behind its Indian peers State Bank of India and ICICI Bank, with market capitalizations of about $62 billion and $79 billion, respectively, as of June 22. </p>.<p>“Worldwide there are very few banks, which can at this scale and size, still aspire to double over a period of four years,” Suresh Ganapathy, head of financial services research for India at Macquarie Group Ltd’s brokerage unit, said in a <em>Bloomberg TV </em>interview. The bank expects to grow at 18 per cent to 20 per cent, there is very good visibility in earnings growth, and they plan to double their branches in the next four years, he said. “HDFC Bank will remain a pretty formidable institution.”</p>.<p><strong>Deposit Growth</strong></p>.<p>HDFC Bank has consistently outperformed its peers in garnering deposits and the merger offers another chance to grow its deposit base by tapping the existing customers of the mortgage lender. Some 70 per cent of those customers do not have accounts with the bank. Arvind Kapil, retail head at the bank, last month said he plans to get them to open a savings account. </p>.<p>The lender will be able to offer inhouse home loan products to its clients as only 2 per cent of them had a mortgage product from HDFC Ltd, according to a presentation when the merger was announced.</p>.<p>“The lifetime value of a customer’s relationship with that bank just enhances when you start to put a mortgage into his product offering,” Sashi Jagdishan, the bank’s chief executive, said at the time. </p>.<p><strong>Confidence Check</strong></p>.<p>HDFC Bank, which counts JPMorgan among its largest investors, is enjoying high levels of investor confidence. Its contingent convertible bonds — the riskiest type of debt that can convert to equity if a lender runs into trouble — has outperformed its global peers. The perpetual dollar notes of HDFC Bank handed investors a return of 3.1 per cent so far this year, even as Bloomberg’s index of global banks’ coco bonds lost 3.5 per cent.</p>.<p>The aggregate index has clawed back some of of its underperformance in recent months after the turmoil caused by a controversial wipeout of Credit Suisse Group AG’s bonds eased. </p>.<p><strong>Stock Performance</strong></p>.<p>HDFC Bank shares are up less than the NIFTY Bank index over the past year. Ganapathy, the Macquarie analyst, reckons the stock’s performance will depend on the growth of the loan book at 18 per cent to 20 per cent, and a 2 per cent return on assets. </p>.<p>“Management is confident of sustaining 2 per cent return on assets and possibly beyond that level even post-merger and also deliver strong loan growth. If they can walk the talk, the stock will re-rate,” Ganapathy said in a note.</p>

_1.png)