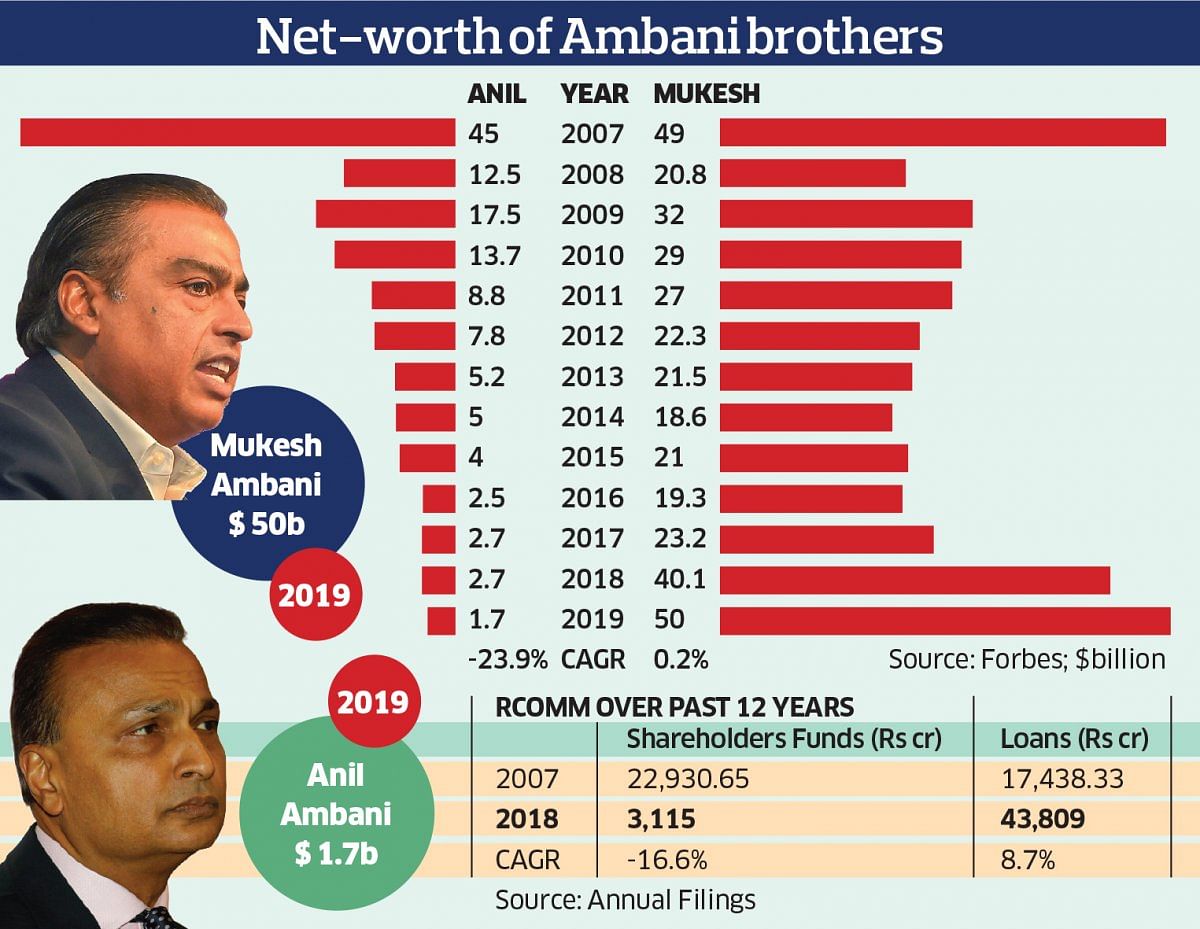

<p>On June 6, 2002, the patriarch of the Reliance Group Dhirubhai Ambani passed away without leaving a will for the multi-crore business empire he had set up from the scratch.</p>.<p>Soon after his death, his two sons, Mukesh Ambani and the younger Anil Ambani got engaged in a bitter battle for the inheritance and control over India’s largest business conglomerate.</p>.<p>It was only when their mother, Kokilaben, brokered a demerger of the group in 2005, which gave Mukesh control of oil and gas, petrochemicals, refining and manufacturing, while Anil took hold over electricity, telecom and financial services – a neat division between the ‘old economy’ and the ‘new economy’.</p>.<p>As both brothers went on to carve their own paths, Mukesh went ahead to become Asia’s richest man, while Anil saw his net-worth plunge multiple times to $1.9 billion, according to Forbes, as on date.</p>.<p>In what could be a big humiliation for Anil, Mukesh set aside the bitter feud to bail his younger brother out of the crisis on the last day of the deadline set by the Supreme Court to clear the dues he owed to Swedish telecom major Ericsson. He owed Rs 580 crore dues to Ericsson. Amid all this financial-family drama, DH spoke to multiple people who have closely worked with Anil Ambani, to understand what went wrong.</p>.<p><strong>Financial Mess </strong></p>.<p>The net-worth of Anil has diminished at an unimaginable rate over the last decade. His current net-worth of $1.7 billion, according to Forbes rich list, is a mere 3.8% of his $45 billion net-worth 12 years ago – a compounded annual decline of 23.9%. On the other hand, Mukesh’s net-worth has risen 102% over the same period.</p>.<p>Just like his personal fortunes, the books of the companies owned by Anil have gone for a toss over the years. At the time of the split between the brothers in 2005, the biggest asset in hand for Anil was his 66% ownership in Reliance Communications (RCom). The holding, over the years, has come down to 53.08%, of which a majority 72.31 crore shares are held by Reliance Communications Enterprises – a privately held company of Anil Ambani.</p>.<p><em><strong>ALSO READ</strong>: </em><a href="https://www.deccanherald.com/national/mukesh-nitas-help-saves-day-for-anil-as-rcom-makes-rs-550-cr-payment-to-ericsson-723957.html" target="_blank"><strong>Mukesh, Nita's help saves day for Anil</strong></a><br /><br /> Since 2007, when Anil’s fortunes started sliding, the shareholders’ funds in his biggest asset – RCom – has seen a compounded decline of 16.6% while debt has grown by a compounded annual growth of 8.7% every year. In March 2007, total shareholders’ funds in RCom stood at Rs 22,930.65 crore, including Rs 21,908.34 crore in reserves and surplus. Fast forward to March 2018 -- while the company’s borrowings, including long-term and current, stood at a whopping Rs 43,807 crore, shareholders’ funds declined to a mere Rs 3,115 crore. In just one year (2017-18), shareholders’ worth declined by 89.2% from Rs 28,969 crore to the current level – mostly on the back of depletion in the reserves, as the company set off its accumulated loss of Rs 23,820 crore.</p>.<p><strong>Everything went wrong</strong></p>.<p>The trouble for Anil started in 2007-8, sparked off by a series of wrong decisions by him. From being the biggest gainer in the Forbes Rich List in 2007, Anil ended up being the biggest loser in the Forbes Rich List in 2008 – when it took a plunge of 72% and has been on the downward trend since.</p>.<p>Back then, Anil had grand plans for RCom. He intended to merge it with South Africa's MTN in what would have been India's largest-ever overseas deal. Only to be scuttled in July 2008, after brother Mukesh threatened to sue, claiming he had the right of first refusal. The stock of RCom tumbled 48% from July 2008 to November 2008, costing Anil a whopping $30 billion of net-worth.</p>.<p>People, who have worked closely with Anil or track him closely attribute his fall to his way of functioning, which includes excessive dependence on debt as a source of capital, autocratic way of functioning, and constant brush with controversial deals, like in the 2G scam and the Rafale deal.</p>.<p>One market advisor, who has been working closely with Anil for years, told DH on condition of anonymity that after his involvement in the 2G affair, he saw his credit lines crunched. “Because of 2G scam, banks stopped funding him in 2011-12. That was the first thing that went wrong for him,” he said.</p>.<p>Yet another senior executive who has formerly worked very closely with Anil said he lacks the patience and endurance that running a business requires. “He has no respect for the professionals in his company. He used to take all decisions himself. Moreover, he doesn’t stick to his business for the long run, like his elder brother. He is too impatient. That is costing him a lot.”</p>.<p>Take the example of Delhi Metro: On January 23, 2008, the DMRC awarded a 30-year build-operate-transfer PPP contract to the Reliance Energy-CAF consortium. It was built at a cost of Rs 5,700 crore, of which Reliance Infra paid Rs 2,885 crore ($580m). Five years later, on June 27, 2013, Reliance Infrastructure communicated to DMRC that they are unable to operate the line beyond June 30, 2013. Following this, DMRC took over operations of Airport Express line from July 1, 2013, with an operations and maintenance team of 100 officials to handle the line. The tale of Yamuna Expressway, which Reliance Infra exited last week, is no different.</p>.<p>According to a former executive of Reliance ADAG Group, yet another bad decision by Anil was to venture into defence, which many people close to him say was aimed at rolling over his bulging debt in the name of big-ticket contracts. “He got taken over by the thing that the government and ruling party is completely in his favour, and they will give him contracts. But the government can’t help him till he has built infrastructure and the capability. He bought the shipyard for his defence business, but that needs to be brought into working condition. Otherwise, it’s useless,” the executive told DH.</p>.<p>Reliance Infrastructure had acquired 17.66% of Pipavav on March 5, 2015 in a $130 million deal. Subsequently, R-Infra launched an open offer to acquire additional shares to control 25.1% of the company. The open offer has been completed and R-Infra now holds 36.5% equity in Pipavav and Anil has been appointed its chairman. The company was then renamed Reliance Defence and Engineering on March 3, 2016, and again renamed Reliance Naval Engineering Limited on September 6, 2017.</p>.<p>Many of his close aides attribute his downfall to venturing into non-core areas. “To save his slide, he ventured into non-core businesses, which cost him further,” a person closely working with all the Reliance ADAG companies said.</p>.<p>The biggest reason for Anil’s downfall, however, has been his excessive dependence on debt. “He has overextended himself. With connections, you get loans. Banks gave the group massive loans. They fund their projects using the loan and then service the loan using profits. Now that he has over-leveraged himself, servicing has become unviable,” multiple people who have closely worked with Anil said.</p>.<p>However, some of those people also said Anil is excellent in number crunching. That is probably why the only business of Reliance ADAG group that has been doing well over the years has been Reliance Capital. During 2017-18, reserves of R-Cap grew from Rs 13,448 crore to Rs 13,915 crore. Similarly, the profits of the company grew from Rs 517 crore to Rs 818 crore.</p>.<p>Mukesh may have saved his younger brother this time, which cost him Rs 462 crore. But a whole train of other lenders and vendors have queued up now to recover dues worth thousands of crores. Can or will Mukesh pay all of them off to keep Anil out of jail?</p>

<p>On June 6, 2002, the patriarch of the Reliance Group Dhirubhai Ambani passed away without leaving a will for the multi-crore business empire he had set up from the scratch.</p>.<p>Soon after his death, his two sons, Mukesh Ambani and the younger Anil Ambani got engaged in a bitter battle for the inheritance and control over India’s largest business conglomerate.</p>.<p>It was only when their mother, Kokilaben, brokered a demerger of the group in 2005, which gave Mukesh control of oil and gas, petrochemicals, refining and manufacturing, while Anil took hold over electricity, telecom and financial services – a neat division between the ‘old economy’ and the ‘new economy’.</p>.<p>As both brothers went on to carve their own paths, Mukesh went ahead to become Asia’s richest man, while Anil saw his net-worth plunge multiple times to $1.9 billion, according to Forbes, as on date.</p>.<p>In what could be a big humiliation for Anil, Mukesh set aside the bitter feud to bail his younger brother out of the crisis on the last day of the deadline set by the Supreme Court to clear the dues he owed to Swedish telecom major Ericsson. He owed Rs 580 crore dues to Ericsson. Amid all this financial-family drama, DH spoke to multiple people who have closely worked with Anil Ambani, to understand what went wrong.</p>.<p><strong>Financial Mess </strong></p>.<p>The net-worth of Anil has diminished at an unimaginable rate over the last decade. His current net-worth of $1.7 billion, according to Forbes rich list, is a mere 3.8% of his $45 billion net-worth 12 years ago – a compounded annual decline of 23.9%. On the other hand, Mukesh’s net-worth has risen 102% over the same period.</p>.<p>Just like his personal fortunes, the books of the companies owned by Anil have gone for a toss over the years. At the time of the split between the brothers in 2005, the biggest asset in hand for Anil was his 66% ownership in Reliance Communications (RCom). The holding, over the years, has come down to 53.08%, of which a majority 72.31 crore shares are held by Reliance Communications Enterprises – a privately held company of Anil Ambani.</p>.<p><em><strong>ALSO READ</strong>: </em><a href="https://www.deccanherald.com/national/mukesh-nitas-help-saves-day-for-anil-as-rcom-makes-rs-550-cr-payment-to-ericsson-723957.html" target="_blank"><strong>Mukesh, Nita's help saves day for Anil</strong></a><br /><br /> Since 2007, when Anil’s fortunes started sliding, the shareholders’ funds in his biggest asset – RCom – has seen a compounded decline of 16.6% while debt has grown by a compounded annual growth of 8.7% every year. In March 2007, total shareholders’ funds in RCom stood at Rs 22,930.65 crore, including Rs 21,908.34 crore in reserves and surplus. Fast forward to March 2018 -- while the company’s borrowings, including long-term and current, stood at a whopping Rs 43,807 crore, shareholders’ funds declined to a mere Rs 3,115 crore. In just one year (2017-18), shareholders’ worth declined by 89.2% from Rs 28,969 crore to the current level – mostly on the back of depletion in the reserves, as the company set off its accumulated loss of Rs 23,820 crore.</p>.<p><strong>Everything went wrong</strong></p>.<p>The trouble for Anil started in 2007-8, sparked off by a series of wrong decisions by him. From being the biggest gainer in the Forbes Rich List in 2007, Anil ended up being the biggest loser in the Forbes Rich List in 2008 – when it took a plunge of 72% and has been on the downward trend since.</p>.<p>Back then, Anil had grand plans for RCom. He intended to merge it with South Africa's MTN in what would have been India's largest-ever overseas deal. Only to be scuttled in July 2008, after brother Mukesh threatened to sue, claiming he had the right of first refusal. The stock of RCom tumbled 48% from July 2008 to November 2008, costing Anil a whopping $30 billion of net-worth.</p>.<p>People, who have worked closely with Anil or track him closely attribute his fall to his way of functioning, which includes excessive dependence on debt as a source of capital, autocratic way of functioning, and constant brush with controversial deals, like in the 2G scam and the Rafale deal.</p>.<p>One market advisor, who has been working closely with Anil for years, told DH on condition of anonymity that after his involvement in the 2G affair, he saw his credit lines crunched. “Because of 2G scam, banks stopped funding him in 2011-12. That was the first thing that went wrong for him,” he said.</p>.<p>Yet another senior executive who has formerly worked very closely with Anil said he lacks the patience and endurance that running a business requires. “He has no respect for the professionals in his company. He used to take all decisions himself. Moreover, he doesn’t stick to his business for the long run, like his elder brother. He is too impatient. That is costing him a lot.”</p>.<p>Take the example of Delhi Metro: On January 23, 2008, the DMRC awarded a 30-year build-operate-transfer PPP contract to the Reliance Energy-CAF consortium. It was built at a cost of Rs 5,700 crore, of which Reliance Infra paid Rs 2,885 crore ($580m). Five years later, on June 27, 2013, Reliance Infrastructure communicated to DMRC that they are unable to operate the line beyond June 30, 2013. Following this, DMRC took over operations of Airport Express line from July 1, 2013, with an operations and maintenance team of 100 officials to handle the line. The tale of Yamuna Expressway, which Reliance Infra exited last week, is no different.</p>.<p>According to a former executive of Reliance ADAG Group, yet another bad decision by Anil was to venture into defence, which many people close to him say was aimed at rolling over his bulging debt in the name of big-ticket contracts. “He got taken over by the thing that the government and ruling party is completely in his favour, and they will give him contracts. But the government can’t help him till he has built infrastructure and the capability. He bought the shipyard for his defence business, but that needs to be brought into working condition. Otherwise, it’s useless,” the executive told DH.</p>.<p>Reliance Infrastructure had acquired 17.66% of Pipavav on March 5, 2015 in a $130 million deal. Subsequently, R-Infra launched an open offer to acquire additional shares to control 25.1% of the company. The open offer has been completed and R-Infra now holds 36.5% equity in Pipavav and Anil has been appointed its chairman. The company was then renamed Reliance Defence and Engineering on March 3, 2016, and again renamed Reliance Naval Engineering Limited on September 6, 2017.</p>.<p>Many of his close aides attribute his downfall to venturing into non-core areas. “To save his slide, he ventured into non-core businesses, which cost him further,” a person closely working with all the Reliance ADAG companies said.</p>.<p>The biggest reason for Anil’s downfall, however, has been his excessive dependence on debt. “He has overextended himself. With connections, you get loans. Banks gave the group massive loans. They fund their projects using the loan and then service the loan using profits. Now that he has over-leveraged himself, servicing has become unviable,” multiple people who have closely worked with Anil said.</p>.<p>However, some of those people also said Anil is excellent in number crunching. That is probably why the only business of Reliance ADAG group that has been doing well over the years has been Reliance Capital. During 2017-18, reserves of R-Cap grew from Rs 13,448 crore to Rs 13,915 crore. Similarly, the profits of the company grew from Rs 517 crore to Rs 818 crore.</p>.<p>Mukesh may have saved his younger brother this time, which cost him Rs 462 crore. But a whole train of other lenders and vendors have queued up now to recover dues worth thousands of crores. Can or will Mukesh pay all of them off to keep Anil out of jail?</p>